‘Lessons from Downtown’ was the theme of the first webinar in the Beauty in Travel Retail event organized by the TFWA in partnership with BW Confidential, which took place on June 14. Topics included the state of the domestic and travel-retail beauty market, how the role of the store is changing, the impact of inflation on consumer spend and key trends in the beauty industry.

NPD on the state of the market

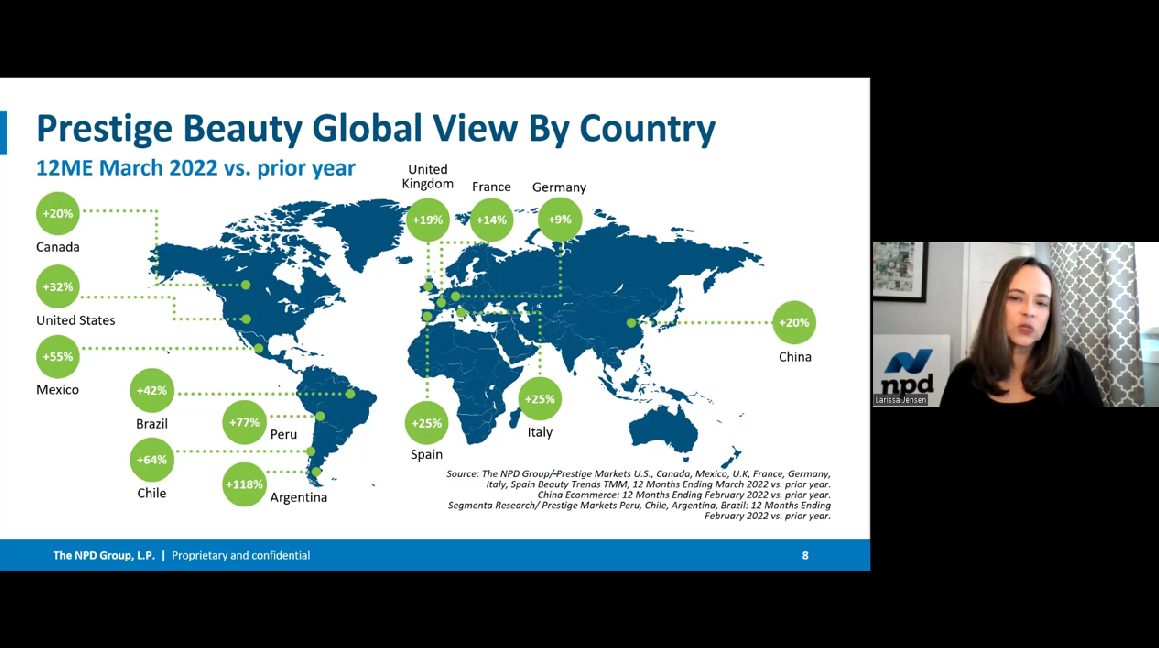

The NPD Group Vice President, Beauty Industry Advisor Larissa Jensen opened the event with data that showed that the beauty category grew two-to-three times the total retail landscape worldwide in 2021 – indicating the industry’s resilience.

While all regions saw growth, the US stood out for its performance in the prestige beauty market in 2021. While Mexico had the strongest growth rate in North America (+55%), the US’ growth (+32%) was the most impressive given the size of the market, noted Jensen.

Across South America dollar growth was strong and units were up double digits. All countries returned to pre-pandemic levels, save for Peru, which closed all retail during lockdown periods, including online.

Meanwhile, in Europe, the strongest growth came from Spain (+25%) and Italy (+25%). While both countries are starting to see the return of tourism, they are still below pre-pandemic levels. The UK (+19%), France (+14%) and Germany (+9%) all had lockdowns during the period which resulted in softer performances.

China, whose sales rose 20% for the year, is beginning to see the impact of a slowing economy.

US fragrance surge

“The biggest surprise in the annual sales results [in the US] is that this is the first time in history that fragrance became the same size of skincare,” Jensen said.

Fragrance was bigger in both department stores and specialty stores in the US than the skincare category, which was driven by a last-minute push during the holiday season.

However, 2022’s results so far show that fragrance’s reign is not holding out. Make-up’s recovery and the premiumization and innovation in haircare is driving growth.

Prestige beauty sales in the US rose 19% year-over-year to $5.3bn in the first three months of the year. Jensen noted that price increases are not driving this performance, outlining that prestige beauty’s units are also growing double digits – a trend that NPD is not seeing in any other discretionary category.

When compared to other industries, beauty’s average price in the US is growing at the lowest rate this year.

So far this year, beauty’s average price increase in the US is 3% to 4%; by comparison, in 2021 prices rose 15% for fragrance. “The huge average price growth was less about price increases and more about consumers spending more on higher-priced items,” Jensen commented. “While overall prices did go up, that big gain in average price was driven more by product choices.”

The percentage of prestige beauty units on promotion, meanwhile declined for the first time in several years in 2021 in the US. These decreases were seen across every beauty category compared to both 2020 and 2019 levels.

This trend is continuing in 2022 for all categories, save for skincare, which is seeing an increase in the number of promotions. Jensen noted that this is what typically happens before a segment begins to decline. This is in part why make-up became so promotional over the past few years, she commented.

Make-up rebounds

Lipstick sales in the US rose 44% in the first quarter of 2022 compared to the same period last year. Lip products grew faster than eye and face products during the period. Other products doing well are blush and bronzer. Additionally, make-up remover sales rose 30% year-over-year during the period, indicating that consumers in the US are flocking back to make-up, claimed Jensen.

Meanwhile, bodycare continued to grow at a faster rate than facial skincare during the first quarter—body care sales were up 26%, while skincare rose 11%. Sunscreen sales rose 60% year-over-year in the first quarter, which is not yet peak season for the segment, noted Jensen.

Meanwhile, fragrance continues to perform well, especially during holidays. For example, Valentine’s Day (February 14) gave a boost to fragrance juice sales (+23%) and the category’s performance was higher than make-up sales.

In haircare, hair styling products, such as gels and hairsprays, are outperforming the category, again showing that consumers are returning to socializing.

Additionally, hair color continues to see growth, even though salons have re-opened in the US. Some 90% of consumers plan to purchase some type of hair product in the next six months, according to NPD data. This intent to use is higher than any other beauty category.

Outlook

Beauty was the only industry with positive unit performance year-to-date as of May in the US across all retail discretionary categories that NPD tracks.

“As of today, our industry has not yet felt the effects of inflationary pressures, but the pressures are there, among many others,” she added.

Headwinds, such as geo-political uncertainty, COVID variants, inflationary pressure and supply-chain issues, may still impact the sector. Nonetheless, in the US consumers are returning to experiences in droves, which beauty stands to benefit from.

“Worldwide we are seeing a rise in the beauty index. While we know of the lipstick and fragrance index, the beauty index is being fueled by a redefinition of wellness, expanded beyond physical wellness to become more about mental wellness,” Jensen said.

The retail view

UK-based retailer Space NK CEO Andy Lightfoot provided insight into the future of online sales, how the role of the store is changing and the impact of inflation on the market. He also talked about the retailer’s new Wholesale Plus model in the US and upcoming trends in beauty.

Read the full interview with Space NK CEO Andy Lightfoot.

Travel retail recovery

Beauty in travel retail is coming back, according to German travel retailer Gebr Heinemann Head of Category Management Jan Binke. While Gebr Heinemann’s sales were down 53% in 2021 compared to 2019, its sales in May were down 28% compared to the same month in 2019. Heinemann predicts 2022 sales to be down 25% compared to 2019 levels and forecasts that the travel-retail industry as a whole will return to 2019 levels by 2024.

Puig Global Travel Retail Vice President Kaatje Noens said its travel-retail business is already at 2019 levels. Noens credited the performance to what she said were risks and partnerships the company took in 2021, such as launching the Paco Rabanne Phantom fragrance exclusively in travel retail, plus the implementation of Penhaligon’s pop-ups throughout the year.

“We do not want to be too naïve. Recovery is better than the pax trend because very affluent passengers are traveling right now, and Gen Z is the vast majority of the travelers out there,” Noens said. “Gen Z consumers spend more than any other travelers. However, the summer season will be very indicative of how the traveler will spend, especially in Europe.”

Niche drives growth

Fragrance is driving beauty’s growth in travel retail, with sales of the category at Heinemann now 80% of 2019 levels.

At Puig, Noens outlined how the company is looking to develop the niche fragrance category. “Travel retail as a platform will be the ultimate flagship for those niche brands,” Noens commented. “Niche always sounds small, but it will be big in numbers and that is what we see right now. The recovery to 2019 levels is partly due to the niche category that we have been doubling down on, and we have just started.”

Binke noted that commercial niche saw stronger demand in Europe, while the high luxury niche is still in selective doors. Nonetheless, the niche spend is also in line with consumers spending more. Heinemann’s average transaction value was higher in 2021, which was led by niche fragrance.

Puig has introduced pop-ups, complemented by digital tools, to drive its niche fragrance roll out in travel retail. Noens noted that niche stands to benefit from travel retail thanks to its in-person, experience-based proposition.

“The ultimate definition that everyone refers to for niche today is a very limited distribution in the local market,” she noted. “People do not have the convenience of discovering these brands just around the corner in their local perfumery. And maybe you do not want to spend your first $300 on a bottle online, but you want to discover it with the full experience.”

“Some travelers are digitally savvy and can use [our digital fragrance tool] Magic Monocle. It is not pushing them to convert to sales immediately, but allows them to discover the brand and products on their own time and purchase when they want,” Noens added.

Targeting the consumer

Binke noted that Heinemann will look to increase the number of interactions it has with consumers to boost store footfall.

“The interactions that we are having at the moment with the customers coming in, we can increase those numbers. One of the numbers we have been talking about is maybe to tenfold the interaction before, during and at the end of the journey,” Binke commented.

“It could be a push notification while waiting to check in for a flight, featuring something interesting for that specific traveler, whether it be a specific product or home delivery offer. We are currently looking at this with the Heinemann loyalty program.”

Similarly, Puig aims to reach the consumer at 10 touchpoints before the passenger even arrives at the airport. This approach includes initiatives on travel platforms, such as airlines’ websites, applications and booking pages, in addition to partnerships with local social-media influencers.

Part of the company’s collaboration with influencers, is to respond to and attract the Gen Z consumer.

“I do not think we need to underestimate the fact that the Gen Z traveler was spending money and traveling more than any other generation,” Noens commented.

In part to attract millennial and Gen Z consumers, Heinemann will be upping its efforts in its clean beauty offer. The retailer launched a clean beauty offer in 2019. It is now available in 40 points of sale and Heinemann will expand it this year by adding make-up to the assortment.

In addition to the clean beauty expansion, the retailer will also focus on adding smaller brands, such as influencer brands, plus doctor skincare brands (Dr. Barbara Sturm and Augustinus Bader) and professional haircare.

Heinemann also has “ambitious goals” to increase its travel-retail exclusive offer, Binke said.

Travel-retail exclusives currently make up 4% of Heinemann’s assortment, a number the retailer aims to grow to between 12% and 15%.

Asked whether the retailer will delist more brands to make room for these new offers, Binke said: “Like everybody else we had to adjust and streamline the assortment in 2020, massively. We already delisted 30% of our brands and our industry partners had to decrease a couple of SKUs, even up to 40% in the make-up category. We already did our fair share of that, but we will find the space for these new brands. We did our homework in 2020 by looking at what customers were actually buying.”

E-commerce development

Noens noted that travel retailers need to ask themselves what objective they are looking to fulfil with their e-commerce operations.

“It can be very transactional – for example, in Asia Pacific travelers do not want to wait in line to pay, so we see a higher demand for click & collect and convenience – or is it about becoming a curator, then you are looking at a totally different element,” Noens stated.

She noted that if the aim is solely to offer travelers convenient shopping methods, the means of communication can be improved. Passengers disconnect when they have to click two or more times, she claimed.

She added that travel retailers should also look at how they can work together with brands to execute their e-commerce strategy.

Inflation outlook

Both Noens and Binke said they have not yet seen an impact of inflation on the business. Binke added however, that this could change in the next six to 12 months.

“For the moment we do not see too much impact today. However, it may start to change during the summer season when families travel more,” Noens noted. “Nonetheless, Gen Z is not holding back and is a vast majority of travelers right.”

Overall, Binke noted that the demand for travel is strong. “There is a high demand for travel and people are at the airport, having a journey there, and we do not see the demand for travel breaking at the moment,” he concluded.